The #1 Niche for Defense Startups: Drones

The #1 Niche for Defense Startups: Drones

In an era where warfare is increasingly defined by autonomy and precision, drones have emerged as the undisputed kingpin for defense startups. As geopolitical tensions simmer—from Ukraine's battlefields to potential Pacific flashpoints—the demand for unmanned aerial vehicles (UAVs) has skyrocketed. These agile, cost-effective systems are reshaping military strategies, offering capabilities that traditional hardware can't match. For entrepreneurs eyeing the defense sector, drones represent the ultimate niche: a blend of cutting-edge tech, massive government contracts, and rapid scalability. With the global military drone market projected to hit $19.25 billion in 2026 and climb to $29.57 billion by 2030 at a CAGR of 11.3%, this space is ripe for innovation and investment. If you are interested to fly a drone in your garden without breaking a bank, you can buy used drones for cheap on open P2P, global marketplaces.M&A and IPO Activity in the UAV/Drone Space

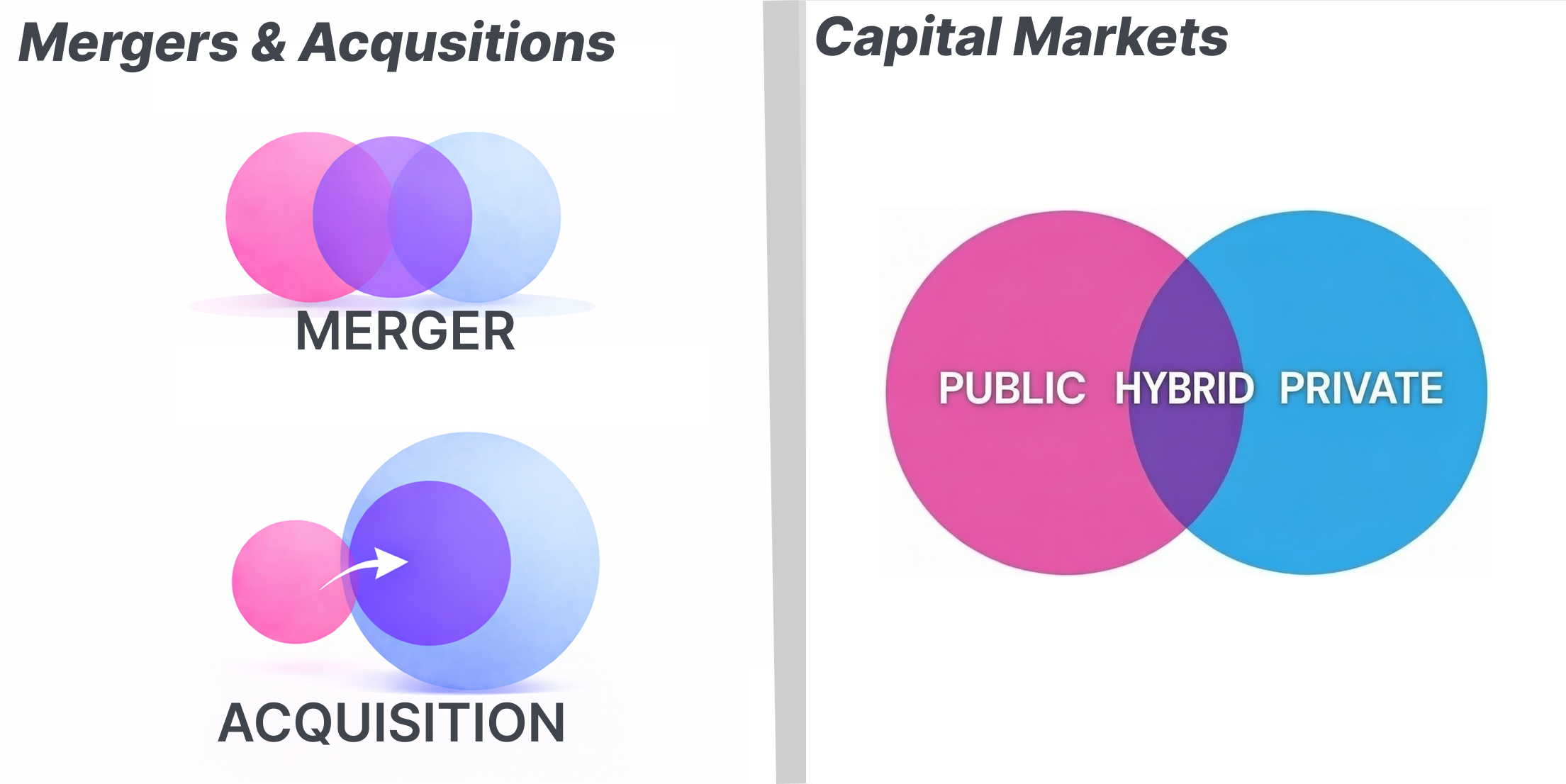

The UAV/drone sector has witnessed a frenzy of mergers and acquisitions (M&A) activity from 2023 to 2026, fueled by escalating geopolitical conflicts, rapid technological advancements, and surging defense budgets. Conflicts in Eastern Europe and the Middle East have underscored drones' pivotal role in modern warfare, prompting a shift toward affordable, autonomous systems. This has driven consolidation as legacy primes and venture-backed firms seek to integrate cutting-edge AI, autonomy, and counter-drone capabilities. In North America alone, drone M&A transactions soared to 46 in 2025, up from 29 in 2024 and 20 in 2023, with a total value of $5.2 billion. Globally, the Air, Land, Sea & Space (ALSS) Systems sector saw 73 deals in YTD 2025, a 35.2% year-over-year increase, with unmanned systems (UxS) like UAVs at the forefront.Notable deals highlight strategic imperatives. In September 2023, Anduril Industries acquired Blue Force Technologies for an undisclosed sum, bolstering its autonomous air vehicle portfolio by integrating AI software Lattice with Fury UAVs. Fast-forward to 2025: Redwire acquired Edge Autonomy Operations for $925 million, enhancing fixed-wing UAV manufacturing for multi-domain operations. Rocket Lab snapped up Mynaric for $150 million in March 2025, adding laser communications resilient to electronic warfare for UAVs. Leonardo's $2 billion acquisition of Iveco Defence Vehicles in July 2025 incorporated UAV and UGV expertise, including NATO contracts for autonomous solutions.

In Europe, Helsing acquired marine tech firm Blue Ocean to extend autonomy into maritime domains. Portuguese Tekever acquired AI aviation software Daedalean for $223 million in August 2025, accelerating GPS-denied drone operations. In the U.S., XTI Aerospace acquired Drone Nerds in November 2025, followed by a $25 million investment from Unusual Machines, targeting VTOL and distribution. Arlington Capital Partners sold BlueHalo to AeroVironment in a blockbuster defense deal exceeding $1 billion.

These transactions reflect trends toward capability-driven consolidation, with strategics acquiring startups for rapid innovation amid U.S. Department of War initiatives like the Drone Dominance Program. Cross-border deals surged 200% in 2025, as bans on Chinese components (e.g., DJI) created market gaps. For startups, M&A offers lucrative exits—venture exits hit $54.4 billion in 2025—but intensifies competition. Looking to 2026, expect more PE involvement and tuck-ins, with counter-drone firms like Chaos Industries (raising $510 million) and Fortem Technologies in focus. This M&A wave underscores drones' transformation from niche to essential, paving the way for broader adoption.

The Rise of Drones in Modern Defense

Drones' ascent began with surveillance but has evolved into a multifaceted force multiplier. Early adopters like the U.S. military used them for reconnaissance, but conflicts in Ukraine and the Middle East have demonstrated their lethality. Cheap, swarming drones can overwhelm defenses, inflicting billions in damage—as seen in Ukraine's "Spider Web" operation, where 117 drones caused $7 billion in Russian losses. This shift favors startups over legacy giants like Lockheed Martin or Boeing, who are bogged down by bureaucratic procurement. Startups thrive on agility, iterating quickly on software-defined systems that integrate AI for autonomous operations.The appeal lies in drones' versatility: intelligence, surveillance, reconnaissance (ISR), precision strikes, electronic warfare, and even logistics. They reduce human risk, operate in GPS-denied environments, and scale affordably. Defense budgets reflect this; the U.S. alone is pouring billions into unmanned systems, with initiatives like the Pentagon's Drone Dominance program aiming to mass-produce low-cost UAVs. For startups, this means opportunities in niche areas like counter-drone tech or swarm coordination, where innovation trumps scale.

Trailblazing Startups Leading the Charge

Success stories abound, proving drones' startup-friendly ecosystem. Anduril Industries, founded by Oculus VR's Palmer Luckey, has become a unicorn with a $30 billion valuation, securing massive contracts for autonomous drones and AI platforms. Their Lattice AI enables drone swarms with minimal human input, positioning them as a disruptor in "unmanned wars."Shield AI, valued at $4 billion, develops "AI pilots" for GPS-denied operations, with products like the V-BAT drone deployed in Ukraine. Skydio, the largest U.S. drone maker, boasts $1.2 billion in bookings, half from defense, offering autonomous alternatives to Chinese dominance. European players like Germany's Quantum Systems and Portugal's Tekever have also hit unicorn status, supplying AI-powered reconnaissance drones to Ukraine.

These firms exemplify the trend: venture capital has poured $204 billion into defense tech since 2021, driven by Ukraine's lessons and China's rise. Startups like Mach Industries focus on cheap, mass-produced drones, echoing the lean startup model of minimum viable products and rapid iteration.

Technological Advancements Fueling Growth

Innovation is the lifeblood of drone startups. AI integration allows autonomous target identification and strikes, as seen in Ukraine where drones use onboard AI for precision attacks. Swarm intelligence enables coordinated fleets, turning individual UAVs into overwhelming forces. Propulsion breakthroughs, like miniaturized turbines and hydrogen fuel cells, extend endurance and reduce noise.Counter-drone tech is booming, with radiofrequency detection and directed energy weapons addressing swarm threats. Open-source software from firms like Auterion accelerates development, allowing hardware-agnostic scaling. These advances lower barriers for startups, enabling them to compete with primes by focusing on software over hardware.

Navigating Challenges in the Drone Space

Despite the hype, hurdles loom. Regulatory compliance, like the U.S. Blue UAS list restricting Chinese components, limits options and raises costs. Supply chain dependencies on China—where DJI holds 70% market share—pose security risks, forcing startups to pivot to domestic sourcing.Talent shortages in AI and cybersecurity, plus long procurement cycles, stifle growth. Battlefield realities, like electronic jamming, demand resilient designs, as Ukraine's experience shows. Startups must balance innovation with manufacturability, outsourcing early R&D to stay lean.

Future Trends: Autonomy and Beyond

Looking to 2026 and beyond, autonomy will dominate. AI-driven swarms, hypersonic integration, and multi-domain operations (air, sea, ground) will redefine warfare. The market could reach $66.5 billion by 2035 at 13.8% CAGR, with emphasis on counter-UAS and quantum-resistant comms.Geopolitical shifts will accelerate adoption; NATO's eastern flank may see AI-powered drone walls. Startups excelling in open architectures and rapid prototyping will thrive, as the U.S. pushes for 48-hour procurement.

Conclusion: Seizing the Drone Revolution

Drones aren't just a niche—they're the future of defense. For startups, the combination of booming demand, technological leaps, and investor enthusiasm creates unparalleled opportunities. Yet success demands navigating regulations, supply chains, and ethical dilemmas like autonomous lethality. As conflicts evolve, those who innovate fastest will lead. With trillions in global defense spending on the line, drones offer startups a shot at reshaping warfare and securing lucrative footholds in this high-stakes arena.

The #1 Niche for Defense Startups: Drones

The #1 Niche for Defense Startups: Drones

In an era where warfare is increasingly defined by autonomy and precision, drones have emerged as the undisputed kingpin for defense startups. As geopolitical tensions simmer—from Ukraine's battlefields to potential Pacific flashpoints—the demand for unmanned aerial vehicles (UAVs) has skyrocketed. These agile, cost-effective systems are reshaping military strategies, offering capabilities that traditional hardware can't match. For entrepreneurs eyeing the defense sector, drones represent the ultimate niche: a blend of cutting-edge tech, massive government contracts, and rapid scalability. With the global military drone market projected to hit $19.25 billion in 2026 and climb to $29.57 billion by 2030 at a CAGR of 11.3%, this space is ripe for innovation and investment. If you are interested to fly a drone in your garden without breaking a bank, you can buy used drones for cheap on open P2P, global marketplaces.M&A and IPO Activity in the UAV/Drone Space

The UAV/drone sector has witnessed a frenzy of mergers and acquisitions (M&A) activity from 2023 to 2026, fueled by escalating geopolitical conflicts, rapid technological advancements, and surging defense budgets. Conflicts in Eastern Europe and the Middle East have underscored drones' pivotal role in modern warfare, prompting a shift toward affordable, autonomous systems. This has driven consolidation as legacy primes and venture-backed firms seek to integrate cutting-edge AI, autonomy, and counter-drone capabilities. In North America alone, drone M&A transactions soared to 46 in 2025, up from 29 in 2024 and 20 in 2023, with a total value of $5.2 billion. Globally, the Air, Land, Sea & Space (ALSS) Systems sector saw 73 deals in YTD 2025, a 35.2% year-over-year increase, with unmanned systems (UxS) like UAVs at the forefront.Notable deals highlight strategic imperatives. In September 2023, Anduril Industries acquired Blue Force Technologies for an undisclosed sum, bolstering its autonomous air vehicle portfolio by integrating AI software Lattice with Fury UAVs. Fast-forward to 2025: Redwire acquired Edge Autonomy Operations for $925 million, enhancing fixed-wing UAV manufacturing for multi-domain operations. Rocket Lab snapped up Mynaric for $150 million in March 2025, adding laser communications resilient to electronic warfare for UAVs. Leonardo's $2 billion acquisition of Iveco Defence Vehicles in July 2025 incorporated UAV and UGV expertise, including NATO contracts for autonomous solutions.

In Europe, Helsing acquired marine tech firm Blue Ocean to extend autonomy into maritime domains. Portuguese Tekever acquired AI aviation software Daedalean for $223 million in August 2025, accelerating GPS-denied drone operations. In the U.S., XTI Aerospace acquired Drone Nerds in November 2025, followed by a $25 million investment from Unusual Machines, targeting VTOL and distribution. Arlington Capital Partners sold BlueHalo to AeroVironment in a blockbuster defense deal exceeding $1 billion.

These transactions reflect trends toward capability-driven consolidation, with strategics acquiring startups for rapid innovation amid U.S. Department of War initiatives like the Drone Dominance Program. Cross-border deals surged 200% in 2025, as bans on Chinese components (e.g., DJI) created market gaps. For startups, M&A offers lucrative exits—venture exits hit $54.4 billion in 2025—but intensifies competition. Looking to 2026, expect more PE involvement and tuck-ins, with counter-drone firms like Chaos Industries (raising $510 million) and Fortem Technologies in focus. This M&A wave underscores drones' transformation from niche to essential, paving the way for broader adoption.

The Rise of Drones in Modern Defense

Drones' ascent began with surveillance but has evolved into a multifaceted force multiplier. Early adopters like the U.S. military used them for reconnaissance, but conflicts in Ukraine and the Middle East have demonstrated their lethality. Cheap, swarming drones can overwhelm defenses, inflicting billions in damage—as seen in Ukraine's "Spider Web" operation, where 117 drones caused $7 billion in Russian losses. This shift favors startups over legacy giants like Lockheed Martin or Boeing, who are bogged down by bureaucratic procurement. Startups thrive on agility, iterating quickly on software-defined systems that integrate AI for autonomous operations.The appeal lies in drones' versatility: intelligence, surveillance, reconnaissance (ISR), precision strikes, electronic warfare, and even logistics. They reduce human risk, operate in GPS-denied environments, and scale affordably. Defense budgets reflect this; the U.S. alone is pouring billions into unmanned systems, with initiatives like the Pentagon's Drone Dominance program aiming to mass-produce low-cost UAVs. For startups, this means opportunities in niche areas like counter-drone tech or swarm coordination, where innovation trumps scale.

Trailblazing Startups Leading the Charge

Success stories abound, proving drones' startup-friendly ecosystem. Anduril Industries, founded by Oculus VR's Palmer Luckey, has become a unicorn with a $30 billion valuation, securing massive contracts for autonomous drones and AI platforms. Their Lattice AI enables drone swarms with minimal human input, positioning them as a disruptor in "unmanned wars."Shield AI, valued at $4 billion, develops "AI pilots" for GPS-denied operations, with products like the V-BAT drone deployed in Ukraine. Skydio, the largest U.S. drone maker, boasts $1.2 billion in bookings, half from defense, offering autonomous alternatives to Chinese dominance. European players like Germany's Quantum Systems and Portugal's Tekever have also hit unicorn status, supplying AI-powered reconnaissance drones to Ukraine.

These firms exemplify the trend: venture capital has poured $204 billion into defense tech since 2021, driven by Ukraine's lessons and China's rise. Startups like Mach Industries focus on cheap, mass-produced drones, echoing the lean startup model of minimum viable products and rapid iteration.

Technological Advancements Fueling Growth

Innovation is the lifeblood of drone startups. AI integration allows autonomous target identification and strikes, as seen in Ukraine where drones use onboard AI for precision attacks. Swarm intelligence enables coordinated fleets, turning individual UAVs into overwhelming forces. Propulsion breakthroughs, like miniaturized turbines and hydrogen fuel cells, extend endurance and reduce noise.Counter-drone tech is booming, with radiofrequency detection and directed energy weapons addressing swarm threats. Open-source software from firms like Auterion accelerates development, allowing hardware-agnostic scaling. These advances lower barriers for startups, enabling them to compete with primes by focusing on software over hardware.

Navigating Challenges in the Drone Space

Despite the hype, hurdles loom. Regulatory compliance, like the U.S. Blue UAS list restricting Chinese components, limits options and raises costs. Supply chain dependencies on China—where DJI holds 70% market share—pose security risks, forcing startups to pivot to domestic sourcing.Talent shortages in AI and cybersecurity, plus long procurement cycles, stifle growth. Battlefield realities, like electronic jamming, demand resilient designs, as Ukraine's experience shows. Startups must balance innovation with manufacturability, outsourcing early R&D to stay lean.

Future Trends: Autonomy and Beyond

Looking to 2026 and beyond, autonomy will dominate. AI-driven swarms, hypersonic integration, and multi-domain operations (air, sea, ground) will redefine warfare. The market could reach $66.5 billion by 2035 at 13.8% CAGR, with emphasis on counter-UAS and quantum-resistant comms.Geopolitical shifts will accelerate adoption; NATO's eastern flank may see AI-powered drone walls. Startups excelling in open architectures and rapid prototyping will thrive, as the U.S. pushes for 48-hour procurement.

Conclusion: Seizing the Drone Revolution

Drones aren't just a niche—they're the future of defense. For startups, the combination of booming demand, technological leaps, and investor enthusiasm creates unparalleled opportunities. Yet success demands navigating regulations, supply chains, and ethical dilemmas like autonomous lethality. As conflicts evolve, those who innovate fastest will lead. With trillions in global defense spending on the line, drones offer startups a shot at reshaping warfare and securing lucrative footholds in this high-stakes arena.